Here’s What to Know About Your Retirement Plan Options

Starting a New Job?

A new job often means a new routine, new colleagues - and new financial decisions. One important piece that sometimes gets buried in the paperwork is your retirement plan. But understanding your options now can help you set a solid foundation for your future.

Here’s a guide to help you make sense of what’s being offered - and how to make the most of it.

Knowing what kind of plan you’re enrolling in is the first step toward aligning it with your broader financial goals.

If your employer offers a matching contribution, don’t leave that money on the table. A typical match might look like this:

“We’ll match 100% of the first 3% you contribute, and 50% of the next 2%.”

This is essentially free money toward your retirement. If your budget allows, try to contribute at least enough to get the full match. It's one of the most effective ways to accelerate your savings.

Some plans offer both Traditional and Roth 401(k) or 403(b) options:

In many cases, a mix of both can provide flexibility down the road.

Once you’re enrolled, your next step is to choose how your money is invested.

Employer plans typically offer a selection of mutual funds, index funds, and target-date funds (which automatically adjust your asset mix as you approach retirement age).

Things to consider:

Some employers let you start contributing to the plan immediately. Others may have a waiting period, often 30 to 90 days, or even up to a year before you're eligible to enroll or receive a company match.

Make sure to:

If you had a retirement plan at your previous job, you’ve got a few options:

Even if you’re not ready to make any big changes, simply understanding your options can give you more confidence and control over your financial future.

Now is a great time to revisit your retirement goals, especially if your income or benefits have changed with the new job.

Retirement planning doesn’t have to be overwhelming. Taking just a little time now -whether that means enrolling in your new plan, adjusting contributions, or getting clarity on the investments - can make a big difference down the road.

If you’re starting a new job or helping a loved one who is, we’re here to help. Let’s review the retirement plan together and see how it fits into your broader financial picture.

Here’s a guide to help you make sense of what’s being offered - and how to make the most of it.

1. Understand What Type of Plan You're Being Offered

Most employers offer a retirement plan known as a defined contribution plan, such as a:- 401(k) – Common in private companies

- 403(b) – Often found in public schools, hospitals, and nonprofits

- 457(b) – Typically offered by government and certain nonprofit employers

- SIMPLE IRA - Frequently offered by small businesses

Knowing what kind of plan you’re enrolling in is the first step toward aligning it with your broader financial goals.

2. Look for a Company Match (and Take Advantage of It!)

If your employer offers a matching contribution, don’t leave that money on the table. A typical match might look like this:

“We’ll match 100% of the first 3% you contribute, and 50% of the next 2%.”

This is essentially free money toward your retirement. If your budget allows, try to contribute at least enough to get the full match. It's one of the most effective ways to accelerate your savings.

3. Is There a Roth Option? It's Worth Exploring

Some plans offer both Traditional and Roth 401(k) or 403(b) options:

- Traditional contributions are pre-tax. You lower your taxable income now but pay taxes when you withdraw in retirement.

- Roth contributions are after-tax. You pay taxes now, but qualified withdrawals later are tax-free.

In many cases, a mix of both can provide flexibility down the road.

4. Review Your Investment Options

Once you’re enrolled, your next step is to choose how your money is invested.

Employer plans typically offer a selection of mutual funds, index funds, and target-date funds (which automatically adjust your asset mix as you approach retirement age).

Things to consider:

- Target-date funds can be a simple, one-fund solution if you prefer a hands-off approach.

- If you’re comfortable being more hands-on, you can build your own portfolio based on risk tolerance, time horizon, and investment preferences.

5. Understand When You're Eligible to Enroll

Some employers let you start contributing to the plan immediately. Others may have a waiting period, often 30 to 90 days, or even up to a year before you're eligible to enroll or receive a company match.

Make sure to:

- Mark your calendar with the date you become eligible

- Log into your plan’s online portal when the time comes

- Set up your contributions and investment elections as soon as you’re able

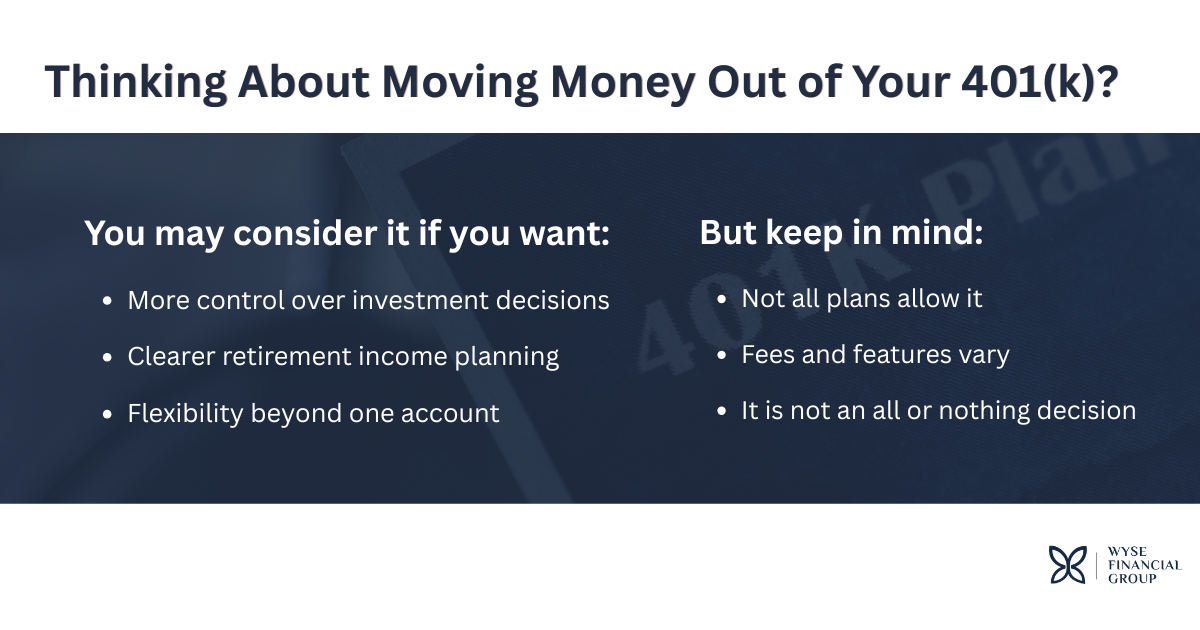

6. Think About What to Do With Your Old Plan

If you had a retirement plan at your previous job, you’ve got a few options:

- Leave it where it is – Many plans allow this, though you’ll no longer be able to contribute

- Roll it into your new employer’s plan – This can simplify things if the new plan has solid investment choices

- Roll it into an IRA – Offers more investment flexibility and keeps your accounts consolidated

7. Take Time to Understand Your Choices

Even if you’re not ready to make any big changes, simply understanding your options can give you more confidence and control over your financial future.

Now is a great time to revisit your retirement goals, especially if your income or benefits have changed with the new job.

Final Thoughts

Retirement planning doesn’t have to be overwhelming. Taking just a little time now -whether that means enrolling in your new plan, adjusting contributions, or getting clarity on the investments - can make a big difference down the road.

If you’re starting a new job or helping a loved one who is, we’re here to help. Let’s review the retirement plan together and see how it fits into your broader financial picture.